The most established name in real estate crowdfunding might actually be the most restrictive choice for your 2026 portfolio. You’ve likely considered fundrise because you value the tangible stability of property over the erratic swings of the public markets. It’s a sensible approach for building long-term wealth and securing a predictable future. However, as the digital finance sector evolves, the traditional five-year lock-up periods that once seemed standard now feel increasingly burdensome compared to new liquidity models.

This comprehensive evaluation explores whether the platform’s legacy REIT structure can compete with the 22% surge in Real World Asset (RWA) tokenization seen since early 2025. You’ll get a transparent look at how management fees impact your final yield and which high-margin niches currently offer the best protection against inflation. We’ll examine the platform’s current performance metrics alongside modern alternatives to help you decide if your capital is truly in the safest possible hands.

Key Takeaways

- Understand the evolution of the eREIT model and how it continues to provide a stable entry point for passive real estate exposure in 2026.

- Evaluate the performance of fundrise against modern benchmarks to determine if its fee structure still supports your long-term wealth goals.

- Gain clarity on the 5-year investment horizon and how to effectively navigate the liquidity constraints inherent in private market assets.

- Compare traditional SEC-regulated funds with innovative RWA tokenization to see which mechanism offers better transparency and security for your capital.

- Determine if your financial profile aligns with the ultra-passive, conservative strategy recommended for the current real estate crowdfunding landscape.

What is Fundrise? Understanding the eREIT Model in 2026

Fundrise stands as a foundational pillar in the digital investment space. Since its launch in 2012, Fundrise has transitioned from a small startup into a multi-billion dollar platform that redefined how individuals interact with institutional-grade assets. It pioneered the eREIT (Electronic Real Estate Investment Trust) model, which allows individual investors to pool their capital into diversified portfolios of commercial and residential properties. Unlike traditional REITs traded on public exchanges, these are private, which helps insulate them from the daily volatility of the stock market.

The platform has effectively democratized access to high-value portfolios that were once reserved for ultra-high-net-worth individuals or pension funds. By 2026, the company has expanded its reach far beyond simple property ownership. It now integrates private credit and venture capital through its Innovation Fund, offering a comprehensive alternative to traditional stock and bond allocations. This evolution reflects a broader trend where investors seek stability through tangible assets and private market growth.

The 2026 shift toward private credit and venture capital represents a strategic response to a changing economic environment. By providing loans to developers and investing in mid-to-late-stage technology companies, the platform offers a multi-layered approach to wealth building. This diversification is designed to provide resilience, ensuring that a portfolio isn’t solely dependent on property appreciation or rental income.

The Core Investment Products

The current product lineup focuses on two primary vehicles. The Flagship Fund targets long-term capital appreciation through a mix of residential and industrial assets. In contrast, the Income Real Estate Fund prioritizes consistent cash flow via debt investments. For those exploring real estate crowdfunding, these funds represent a balanced approach to risk management. They serve as a hedge against inflation, providing tangible value when equity markets become unpredictable. These products are particularly suited for investors with a five-to-ten-year time horizon who value steady, compounding growth over speculative gains.

Account Levels and Minimums

Accessibility remains a core tenet of the fundrise experience. The account tiers are structured to accommodate different stages of an investor’s journey:

- Starter: Requires a $10 minimum. It’s designed for those testing the waters with a diversified portfolio of real estate and venture assets.

- Basic: At a $1,000 minimum, this tier unlocks access to IRAs and the ability to choose specific investment goals, such as supplemental income or long-term growth.

- Premium: This level requires $100,000. It provides access to specialized private equity offerings and direct investment opportunities that offer higher potential returns for accredited and sophisticated investors.

While the platform is open to non-accredited investors, certain specialized funds within the Premium tier remain restricted to those meeting specific net worth or income requirements. This tiered structure ensures that the platform remains inclusive while providing advanced tools for seasoned capital allocators.

Analyzing Fundrise Performance: Fees, Returns, and Risks

Fundrise has built its reputation on the premise that private real estate offers a buffer against stock market volatility. By the start of 2026, data suggests this gap remains visible. While the S&P 500 often experiences double-digit swings based on tech sector sentiment, fundrise portfolios have historically targeted more consistent, albeit often lower, annual returns. During the high-inflation period of 2023 and 2024, the platform’s focus on residential housing and industrial logistics helped it outperform many publicly traded REITs, which are often more sensitive to daily market panic.

The platform’s resilience is tested during interest rate hikes. When the Federal Reserve adjusted rates throughout 2024 and 2025, commercial real estate faced a significant valuation squeeze. Fundrise mitigated this by maintaining lower leverage ratios than traditional institutional investors. This conservative stance means the platform doesn’t always capture the full “peak” of a bull market, but it protects the principal during cyclical downturns.

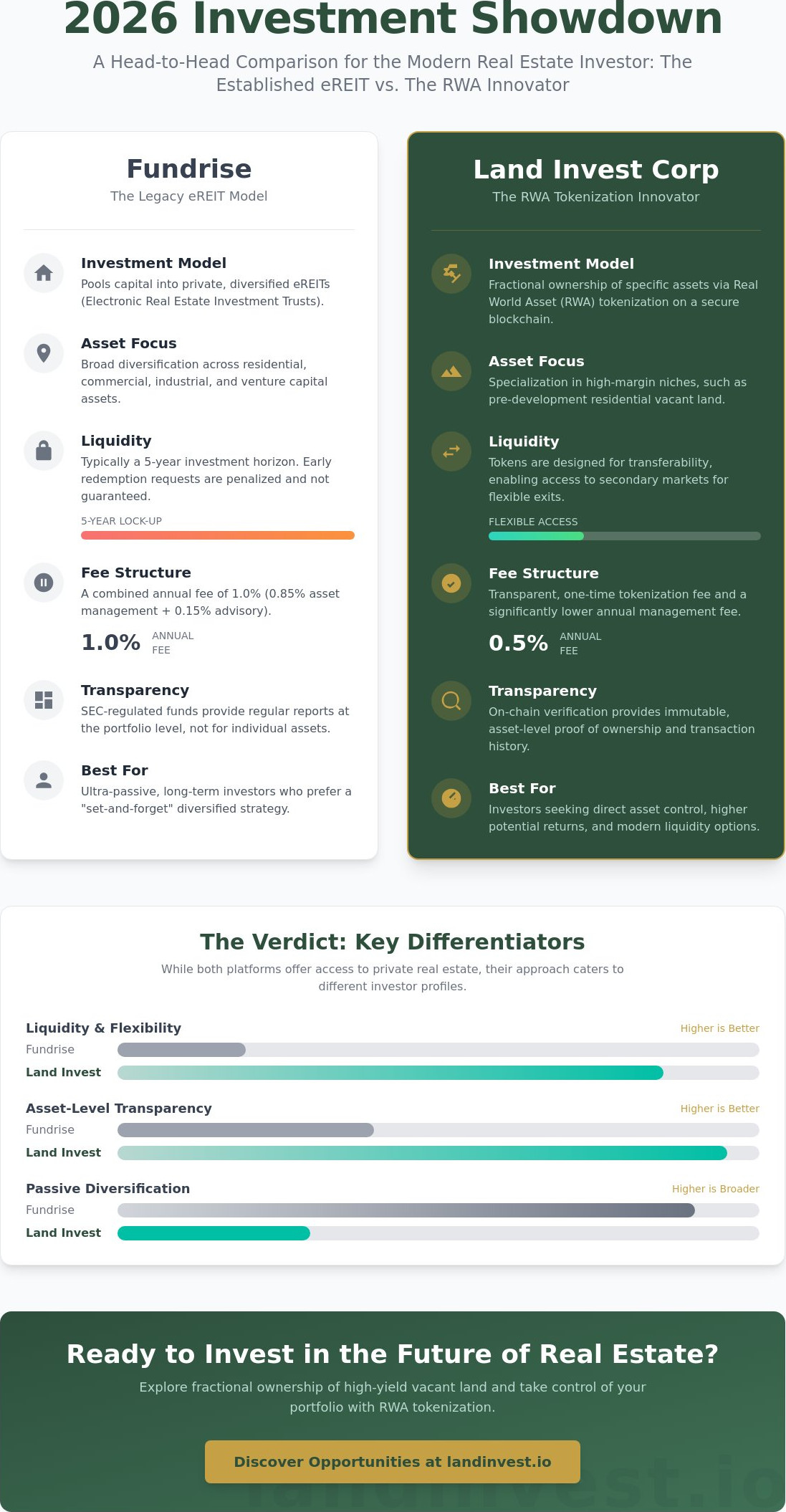

The 1% Fee Structure Explained

Transparency is a core pillar of the platform’s appeal. Investors pay a flat 0.85% annual asset management fee to cover the operating costs of the underlying properties. This includes everything from property taxes to maintenance and tenant management. An additional 0.15% investment advisory fee handles the platform’s technology, reporting, and client services. While a total 1% fee is lower than the traditional “2 and 20” hedge fund model, it’s essential to compare this to modern alternatives. For instance, tokenized real estate platforms often utilize blockchain to reduce these administrative layers even further. For a fundrise investor, the 1% fee is the price paid for a hands-off, curated experience.

Dividend Yield vs. Capital Appreciation

Income generation on the platform usually takes two distinct forms. Quarterly dividends come from rental income, while capital appreciation reflects the increase in the Net Asset Value (NAV) of the properties. Growth-oriented portfolios focus on development projects where the payout happens at the end of a multi-year cycle. This is a slower process than high-velocity strategies like land flipping, which prioritizes quick turnarounds through rezoning or basic improvements. Investors seeking immediate cash flow should prioritize the Income Real Estate Fund, which historically yields higher quarterly distributions than the Flagship Fund.

- Management Fee: 0.85% for property-level operations.

- Advisory Fee: 0.15% for account management.

- Liquidity: Real estate is inherently illiquid; expect a 5-year minimum horizon.

- Risk: Commercial cycles and interest rate sensitivity remain the primary threats.

For those seeking even more stability outside of the residential and commercial sectors, looking into tangible land assets can provide a non-correlated hedge against urban market volatility. Understanding these fee layers and return drivers is the only way to determine if the platform fits your long-term financial goals.

The Liquidity Challenge: Can You Get Your Money Out?

Private real estate is a physical asset class. Unlike stocks that trade in milliseconds, buildings take months or years to buy, renovate, and sell. This fundamental reality means fundrise is not a liquid investment. When you commit capital to the platform, you’re entering a long-term partnership. The company explicitly recommends a minimum five-year investment horizon. This isn’t a suggestion; it’s a structural necessity. Capital is used to fund construction or stabilize multi-family units, and pulling that money out prematurely disrupts the entire portfolio’s health.

If you need to access your cash before the five-year mark, you’ll likely face a “haircut.” This is an early redemption penalty that typically sits around 1% of your share value. While 1% might seem small, it eats into your total returns. It’s a mechanism designed to discourage short-term flipping and to protect long-term investors from the costs associated with constant capital churn. You should only invest money that you won’t need for an emergency or a major purchase in the near future.

Redemption Windows and Restrictions

Fundrise operates on a quarterly redemption cycle. If you want to sell your shares, you must submit a request during specific windows. The board then reviews these requests. It’s vital to understand that approval isn’t automatic. The platform reserves the right to “gate” or suspend redemptions entirely during periods of extreme market volatility or economic distress. We saw this happen across the industry during the 2020 pandemic. This safeguard prevents the fund from being forced to sell properties at a loss just to satisfy a sudden wave of withdrawal requests. Your passive income might arrive regularly, but your principal is effectively tucked away behind a locked door.

Fundrise vs. Secondary Markets

One major limitation is the lack of a secondary market. You can’t list your shares on a public exchange or sell them directly to another user. You’re entirely dependent on the platform’s internal redemption program. This creates a stark contrast with newer models, such as fractional land ownership tokens, which often leverage blockchain technology to facilitate peer-to-peer trading. While fundrise offers a more traditional, stable structure, it lacks that modern flexibility. Liquidity is the primary trade-off for higher private-market yields. Investors comparing token-based platforms should also review our lofty review for 2026 to understand how fractional residential rental tokens handle liquidity differently than land-backed equity offerings. For a broader perspective on how traditional crowdfunding platforms handle these same lock-up constraints, the CrowdStreet review for 2026 offers a direct comparison between established marketplace models and tokenized land equity alternatives.

- Holding Period: 5+ years recommended.

- Redemption Frequency: Quarterly, subject to board approval.

- Early Exit Fee: Approximately 1% if held under 5 years.

- Market Access: No secondary or peer-to-peer trading available.

Investors should view their account as a “set it and forget it” vehicle. Trying to time the real estate market through a crowdfunding platform is a losing strategy. The value comes from the steady appreciation and dividends over years, not from the ability to exit during a price spike.

Fundrise vs. Land Invest Corp: Comparison for 2026

Fundrise remains a reliable choice for broad market exposure, yet it operates on a model designed for a different economic era. While fundrise focuses on institutional-scale commercial and residential developments, Land Invest Corp prioritizes the inherent value of the earth itself. The two platforms represent different philosophies in the 2026 investment landscape. Fundrise manages massive, diversified portfolios through traditional SEC-regulated eREITs. In contrast, Land Invest Corp utilizes Security Token Offerings (STO) to offer fractional equity in specific, high-margin land parcels.

The investor experience differs significantly between the two. A typical fundrise user interacts with a polished app-based dashboard that tracks a broad basket of assets. This is suitable for passive investors who want a hands-off approach. Land Invest Corp appeals to those seeking transparency and direct ownership. By using blockchain verification, every share of equity is recorded on an immutable ledger. This provides a level of security that traditional private equity structures can’t match, as it eliminates the need for middleman verification and reduces administrative friction.

Why Vacant Land is Outperforming REITs

Traditional REITs often struggle with rising maintenance costs, tenant turnover, and complex property management. These factors eat into profit margins over time. The modern vacant land marketplace offers a low-overhead alternative. Land Invest Corp identifies undervalued residential parcels nationwide, focusing on areas where infrastructure expansion is imminent. Because there are no buildings to repair or tenants to manage, the capital remains productive. The speed of the “flip” cycle is also a key differentiator. While a multi-year construction project might take 5 years to yield results, land flipping often realizes gains within 8 to 14 months.

Tokenization: The Technical Edge

Land Invest Corp uses Real World Asset (RWA) tokenization to modernize the investment process. This isn’t about speculative crypto assets; it’s about using blockchain as a digital deed. This technical edge allows for fractional equity that’s easily verifiable and highly secure. STOs provide a more robust compliance framework than older crowdfunding models because they integrate regulatory requirements directly into the smart contract. This ensures that only verified investors participate while providing a clear, transparent audit trail for every transaction. It’s a professional evolution that brings the stability of land into the digital age.

The Verdict: Is Fundrise Right for Your 2026 Portfolio?

Fundrise remains a cornerstone for retail investors in 2026. Its primary strength lies in its battle-tested stability and a user interface that simplifies complex asset management. The platform has successfully navigated multiple market cycles, proving its resilience when traditional equities fluctuated. If you’re a long-term beginner who prefers a “set-and-forget” approach, fundrise is likely your best fit. It provides broad exposure to diversified pools of residential and commercial assets without requiring daily oversight or deep real estate expertise.

However, the 2026 investment environment rewards those who seek specialized growth. If you’re a tech-savvy investor looking for more than just a generic REIT structure, Land Invest Corp offers a compelling alternative. While fundrise manages broad portfolios, Land Invest Corp focuses on the intrinsic value of raw land and agricultural equity. This niche focus provides a hedge against the volatility often found in traditional housing markets. Diversifying across both platforms allows you to balance the steady income of established properties with the high-growth potential of land development. This dual-platform approach ensures you aren’t over-exposed to a single sector of the real estate market.

Building a Modern Real Estate Strategy

A resilient 2026 portfolio shouldn’t rely on a single asset class. Successful investors are now combining broad market exposure with specific land equity to maximize safety. Due diligence is more critical than ever; you must look beyond surface-level yields. Market data from the previous fiscal year showed that portfolios with at least 12% allocation to non-correlated assets like land outperformed pure residential strategies by 3.8%. Your first step should always be education. Understand how land value appreciates differently than developed property before you allocate capital. A well-rounded strategy prioritizes capital preservation as much as it does profit.

Next Steps for Land Investors

Evaluating a land portfolio requires a different lens than assessing a multi-family apartment complex. You’ll want to examine soil quality, zoning potential, and proximity to infrastructure. Land Invest Corp simplifies this through the Security Token Offering (STO) process. This method uses blockchain technology to provide fractional equity, making high-value land accessible with lower entry costs. It’s a transparent way to track ownership and potential returns in real-time. To see this in action, you can explore how Land Invest Corp is evolving real estate through tokenization and determine if land equity fits your risk profile. This transition toward digital equity represents the next logical step for the modern, diversified investor.

Navigating Your Real Estate Strategy for 2026 and Beyond

The landscape of real estate crowdfunding has shifted significantly since the early 2020s. While fundrise remains a prominent name for those seeking exposure to diversified commercial and residential portfolios, the 2026 market demands higher transparency and better liquidity options. Investors often find themselves locked into five year redemption schedules, which can be restrictive during economic shifts. Building a resilient portfolio requires looking ahead at how technology and physical assets intersect.

Current trends show a move toward Real World Asset (RWA) tokenization to solve these traditional bottlenecks. By combining the stability of land with blockchain technology, platforms now offer a more modern approach to fractional equity. Choosing a compliant Security Token Offering (STO) ensures that your digital assets are backed by a strategic, nationwide residential land portfolio. This evolution provides the security of tangible property with the efficiency of modern finance.

Join the future of land investing with Land Invest Corp and secure your wealth through modern RWA tokenization. It’s time to embrace the stability of the ground beneath your feet and move toward a more liquid, transparent investment future.

Frequently Asked Questions

Is Fundrise safe to invest in during 2026?

Fundrise remains a regulated investment platform that operates under SEC oversight and manages over $7 billion in assets for 500,000 active investors as of early 2026. The platform’s security comes from its focus on tangible residential and industrial properties rather than speculative digital assets. While all investing involves risk, the company’s long track record since 2012 provides a foundation of stability for those seeking long-term growth.

What is the minimum investment for Fundrise?

You can start building a real estate portfolio with Fundrise for a minimum of $10. This low entry point allows 1.9 million registered users to access private real estate markets that were previously reserved for institutional investors. By keeping the initial capital requirement low, the platform makes it possible to begin diversifying your wealth without needing tens of thousands of dollars upfront.

How does Fundrise compare to a traditional REIT?

Fundrise utilizes non-traded eREITs, which differ from traditional REITs because they aren’t bought or sold on public stock exchanges like the NYSE. This means your fundrise investment isn’t subject to daily stock market volatility or emotional trading spikes. Instead, the share value tracks the actual appraisal of the underlying properties, providing a much smoother performance curve than typical public real estate stocks.

Can I lose money on Fundrise?

Yes, it’s possible to lose money because real estate values fluctuate based on interest rates and broader economic conditions. During the market adjustments of 2023, some private real estate funds experienced a 5% to 10% decrease in net asset value. Since these are equity-based investments, your principal isn’t insured by the FDIC, so you should only invest capital you don’t need for at least five years.

How long is the lock-up period for Fundrise investments?

Fundrise is built for a five-year investment horizon to allow property appreciation and development projects to mature. While the platform offers a quarterly redemption program, it’s not guaranteed and often carries a 1% to 3% penalty for shares held less than five years. This structure protects the community of investors by preventing forced property sales during temporary market downturns.

Does Fundrise offer a secondary market for shares?

No, Fundrise doesn’t provide a secondary market where investors can trade shares directly with one another. Liquidity is managed through the company’s own buyback program, which occurs on a quarterly basis. This lack of a secondary market is a deliberate choice to maintain stability and ensure that the platform’s focus remains on long-term asset management rather than short-term speculation.

What is the difference between Fundrise and Land Invest Corp?

The primary difference lies in the asset class, as fundrise focuses on buildings while Land Invest Corp specializes in agricultural land. Farmland has delivered an average annual return of 10.2% between 1991 and 2023, often outperforming commercial real estate during inflationary periods. While Fundrise offers exposure to housing and warehouses, Land Invest Corp provides a hedge through the essential nature of food production and soil value.

Are Fundrise dividends taxable as ordinary income?

Most dividends from the platform are taxed as ordinary income because they’re classified as non-qualified dividends on your Form 1099-DIV. However, investors often qualify for the Section 199A deduction, which allows you to deduct up to 20% of qualified REIT dividends from your taxable income. You should consult a tax professional to see how these distributions affect your specific 2026 tax filing requirements.